Report - No Bailouts for Big Tech Billionaires: Policies for when the AI bubble bursts

Overview

Twenty years ago, the U.S. economy morphed into a huge bet on the frothy housing market. The bubble’s animating narrative was simple: housing prices had been rising for a long time, and they would continue to do so. Enticed by the fees they earned for originating mortgages and selling them to banks, lenders increasingly extended credit to borrowers who, as even a cursory look through their finances would have revealed, simply were not earning enough money to cover the debts they were assuming. The result was a classic speculative bubble, the size and risks of which were largely hidden from policymakers due to lax transparency requirements, deceptive accounting, and the fact that much of the riskiest debt had been disguised through financial chicanery and a largely unregulated shadow banking sector.

Despite numerous warning signs, policymakers did not wake up to the danger until the financial system started to unravel. Fearing that inaction would wreck the economy, policymakers orchestrated a series of escalating bailouts, starting with Bear Stearns, followed by Fannie Mae and Freddie Mac, then AIG, and finally Wall Street as a whole. Bailout funds, with extremely favorable conditions for the distressed companies, went to some of the largest and most powerful corporations in the world and were pushed through with little opportunity for public input. Public outrage to the bailouts followed, but the damage — not only to the economy, but to policymakers’ credibility — had been done.

Today, the economy again resembles a huge bet on a market that bears all the signs of a speculative bubble, this time centered on the artificial intelligence (AI) industry. Companies are spending trillions (yes, trillions) of dollars on infrastructure and resources to develop, train, and run generative AI models, particularly chatbots powered by large language models (LLMs).[1] AI companies are taking on massive amounts of debt to finance their spending even though the revenues from selling generative AI products and services would have to grow by orders of magnitude within the next few years to pay those debts. The extent of the risk is, once again, difficult to determine because of poor transparency, deceptive accounting, and the heavy involvement of the shadow banking sector.

Perhaps recognizing the precariousness of their situation, some industry actors have already started dropping hints that the industry might seek government assistance. In November 2025, OpenAI Chief Financial Officer Sarah Friar floated a federal government “backstop” for AI infrastructure investments, citing AI’s economic importance and the need for the U.S. to maintain its technological lead over China, before walking her comments back after public outrage.[2] Weeks later, venture capitalist and White House AI Czar David Sacks tweeted: "AI-related investment accounts for half of GDP growth. A reversal would risk recession. We can’t afford to go backwards.”[3]

These are not the sort of statements one would expect from people confident about their industry’s financial strength. They are, however, exactly what one might expect from people who suspect their industry will need a bailout in the not-too-distant future.

The AI bailout movement thus has begun, albeit in a quiet and veiled form. We should expect AI bailout pleas to increase in frequency and urgency if and when it becomes apparent that the bubble has burst and the promised AI revolution will take longer than promised to arrive. And that’s assuming it ever arrives at all.

Even if arguments for an AI bailout had merit, politicians would have ample reason to be wary of them. The bailouts in the wake of the last financial crisis proved unpopular across the political spectrum.[4] The data centers at the heart of the current bubble are already becoming a magnet for political opposition in many communities, as even the tech industry has been forced to admit.[5] Providing a bailout to a deeply unpopular industry because it overspent on deeply unpopular infrastructure would be, well, deeply unpopular.

Fortunately, this is a case where good politics and good policy align. The goal of this report is to analyze the arguments that could be (and in some cases have been) advanced in favor of an AI industry bailout and explain why they are meritless. My hope is that, armed with this report, policymakers will be able to recognize AI bailout requests for what they are: the self-serving efforts of powerful corporations to make others absorb the losses from their dubious gamble

TABLE OF CONTENTS

Overview

Part I: The AI Bubble

A. Bubble fuel: AI hype

B. Anatomy of the bubble: Everything’s big but the revenues

Part II: What are Bailouts?

A. Block framework

B. A brief history of bailouts

C. Bailout consequences: The big get bigger and the rich get richer

D. Bailout justifications

Part III: Rebutting (and Prebutting) the AI Industry’s Bailout Arguments

A. Importance arguments

B. Worthiness arguments

Part IV: What We Should Do Instead

A. Let failing companies fail

B. Rescue the real economy

C. Prevent a recurrence

Conclusion

Credits

Author

Matthew U. Scherer

Project Director

Courtney Radsch

Contributors

Anita Jain

Sandeep Vaheesan

Max Von Thun

Acknowledgements

The author thanks Advait Arun, Brian Chen, Damon Silvers, Jake Snow, and Shu Dar Yao for their feedback and support.

Epigraph

We have created an ersatz capitalism, socializing losses as we privatize gains, a system with unclear rules, but with a predictable outcome: future crises and undue risk-taking at public expense.

- Joseph Stiglitz, 2010

Overview

Twenty years ago, the U.S. economy morphed into a huge bet on the frothy housing market. The bubble’s animating narrative was simple: housing prices had been rising for a long time, and they would continue to do so. Enticed by the fees they earned for originating mortgages and selling them to banks, lenders increasingly extended credit to borrowers who, as even a cursory look through their finances would have revealed, simply were not earning enough money to cover the debts they were assuming. The result was a classic speculative bubble, the size and risks of which were largely hidden from policymakers due to lax transparency requirements, deceptive accounting, and the fact that much of the riskiest debt had been disguised through financial chicanery and a largely unregulated shadow banking sector.

Despite numerous warning signs, policymakers did not wake up to the danger until the financial system started to unravel. Fearing that inaction would wreck the economy, policymakers orchestrated a series of escalating bailouts, starting with Bear Stearns, followed by Fannie Mae and Freddie Mac, then AIG, and finally Wall Street as a whole. Bailout funds, with extremely favorable conditions for the distressed companies, went to some of the largest and most powerful corporations in the world and were pushed through with little opportunity for public input. Public outrage to the bailouts followed, but the damage — not only to the economy, but to policymakers’ credibility — had been done.

Today, the economy again resembles a huge bet on a market that bears all the signs of a speculative bubble, this time centered on the artificial intelligence (AI) industry. Companies are spending trillions (yes, trillions) of dollars on infrastructure and resources to develop, train, and run generative AI models, particularly chatbots powered by large language models (LLMs).[1] AI companies are taking on massive amounts of debt to finance their spending even though the revenues from selling generative AI products and services would have to grow by orders of magnitude within the next few years to pay those debts. The extent of the risk is, once again, difficult to determine because of poor transparency, deceptive accounting, and the heavy involvement of the shadow banking sector.

Perhaps recognizing the precariousness of their situation, some industry actors have already started dropping hints that the industry might seek government assistance. In November 2025, OpenAI Chief Financial Officer Sarah Friar floated a federal government “backstop” for AI infrastructure investments, citing AI’s economic importance and the need for the U.S. to maintain its technological lead over China, before walking her comments back after public outrage.[2] Weeks later, venture capitalist and White House AI Czar David Sacks tweeted: "AI-related investment accounts for half of GDP growth. A reversal would risk recession. We can’t afford to go backwards.”[3]

These are not the sort of statements one would expect from people confident about their industry’s financial strength. They are, however, exactly what one might expect from people who suspect their industry will need a bailout in the not-too-distant future.

The AI bailout movement thus has begun, albeit in a quiet and veiled form. We should expect AI bailout pleas to increase in frequency and urgency if and when it becomes apparent that the bubble has burst and the promised AI revolution will take longer than promised to arrive. And that’s assuming it ever arrives at all.

Even if arguments for an AI bailout had merit, politicians would have ample reason to be wary of them. The bailouts in the wake of the last financial crisis proved unpopular across the political spectrum.[4] The data centers at the heart of the current bubble are already becoming a magnet for political opposition in many communities, as even the tech industry has been forced to admit.[5] Providing a bailout to a deeply unpopular industry because it overspent on deeply unpopular infrastructure would be, well, deeply unpopular.

Fortunately, this is a case where good politics and good policy align. The goal of this report is to analyze the arguments that could be (and in some cases have been) advanced in favor of an AI industry bailout and explain why they are meritless. My hope is that, armed with this report, policymakers will be able to recognize AI bailout requests for what they are: the self-serving efforts of powerful corporations to make others absorb the losses from their dubious gamble.

For purposes of this report, “AI industry” is an umbrella term encompassing the many companies involved in the interconnected parts of the AI development, training, and operation pipeline, including:

- “Pure play” AI model development companies like OpenAI and Anthropic that focus exclusively on developing their own AI models.

- Big Tech conglomerates that develop their own AI models, most notably Google and Meta. Amazon and Microsoft also develop their own AI models, though they are not in widespread use.

- Companies offering AI products and services using models developed by others.

- Chip developers that produce the hardware used to train and run AI models, most notably Nvidia.

- Cloud service providers, including legacy providers like Amazon Web Services, Microsoft Azure, Google Cloud, and Oracle, as well as AI-focused “neocloud” providers like CoreWeave and Nebius.

- Data center and infrastructure companies that build, operate, or lease the facilities that physically house cloud services and AI infrastructure.

- Financial institutions, particularly venture capital and private credit firms, that help finance these companies’ activities.

This report focuses on the U.S. AI industry and its implications for U.S. policy.

Part I provides an overview of the AI bubble, starting with the narrative hype that has inflated it. It continues with a high-level overview of the bubble’s key economic features, starting with the remarkable valuations of AI-focused tech companies, in which more wealth is tied up than any single industry in history. The report then describes how AI companies are rapidly accumulating debt as they continue to spend orders of magnitude more than they generate in revenues and analyzes the suspect accounting practices that the AI industry is using to obscure its precarious finances.

Part II describes the characteristic features of a bailout using the framework proposed by legal scholar Cheryl Block, who categorized bailouts into overt (like purchases of stock and loan guarantees) and covert (like relief from taxes or other legal obligations) forms. It then provides a brief history of federal government bailouts, highlighting the justifications that were made for each. Those justifications serve as the focus of Part II’s final section, which observes that bailouts are usually justified by a combination of arguments relating to the bailed-out companies’ importance (such as being too big or strategically important to fail, or the possibility that a company’s collapse will cause economic contagion) and worthiness (typically that the companies are financially sound and/or were innocent victims of some external shock).

Part III describes the arguments AI companies will most likely advance to seek a bailout when the AI bubble bursts and rebuts each argument in turn. Briefly, I argue that the AI industry, its hype notwithstanding, is neither strategically important nor vital to the U.S. economy; that tech companies are not like banks, and their collapse would not pose a comparable risk of financial contagion; and that any negative consequences that follow from an AI crash would be better dealt with through other policy approaches. Part IV briefly describes some of those approaches, although a fulsome exploration of those measures is outside the scope of this report.[7]

The report concludes with a reminder of the reason why bailouts are almost always the wrong response to manmade economic crises: such bailouts undermine confidence in democratic institutions while encouraging the sort of excessive risk-taking that sows the seeds for even more severe crises in the future.

Part I: The AI Bubble

A. Bubble fuel: AI hype

In their 2019 book Bubbles and Crashes,[8] Brent Goldfarb and David Kirsch analyzed the history of bubbles and identified four key factors that drive their formation. One of those factors is the creation of powerful narratives around new technologies, particularly narratives that “foster an illusion of inevitability” about a technology’s revolutionary potential.[9] Such narratives tend to be self-reinforcing. “The more people who jump on a particular narrative’s bandwagon, the more real this illusion seems and even becomes,”[10] Goldfarb and Kirsch write. The problem with such narratives is that they lead investors to overlook a technology’s shortcomings.

If narratives are bubble fuel, then generative AI’s tank is overflowing. As New York Times journalist David Streitfeld summarized:

Silicon Valley executives promise that artificial intelligence is going to radically change everyone’s life for the better, starting just a few minutes from now. A.I. is described as the new electricity. It’s even bigger than fire. Don’t bother saving money for retirement because everyone will be rich rich rich.[11]

Such hype has been building for over a decade. As far back as 2015, commentators were talking about AI and related technologies as having the potential to bring about a “Fourth Industrial Revolution” matching or exceeding in importance the advances in manufacturing, electricity, and information technology that defined prior economic transformations. After the arrival of ChatGPT on November 30, 2022, these narratives coalesced around LLM-driven chatbots and related generative AI systems.

Leveraging public awe at LLMs’ ability to output fluent text, AI boosters have argued that the technology is approaching what could be considered “artificial general intelligence” (AGI), a once-fringe and still ill-defined term for technology capable of matching humans in all cognitive tasks. An even more obscure term, superintelligence, used to describe AI systems that will vastly exceed human capabilities in every meaningful way, soon entered common parlance as well. In 2025, Meta renamed its frontier AI research program the “Superintelligence Lab.”

Not content with suggesting that a technological revolution is inevitable or imminent, AI industry leaders have increasingly taken to claiming that it has already begun. In 2023, a Google Vice President asserted that AGI had been achieved,[12] a claim that Nvidia CEO Jensen Huang repeated earlier this year.[13] OpenAI CEO Sam Altman suggested in 2024 that superintelligence would be reached within “a few thousand days.”[14] Shortly before the release of GPT-5 in August 2025, he said that talking to the new version of ChatGPT would be like talking to “a legitimate PhD-level expert in anything, any area you need.”[15]

The hype is not limited to abstract characterizations of AI capabilities. The AI industry is pushing the narrative that AI can already perform the jobs of millions of workers or will soon be able to do so. In a remarkably specific prediction, Anthropic CEO Dario Amodei said in March 2025 that over 90% of code would be written by AI within three to six months.[16] The failure of that and similar forecasts seems to have little effect. Earlier this year, Microsoft AI chief Mustafa Suleyman claimed that “most, if not all” professional white-collar tasks will be “fully automated by an AI within the next 12 to 18 months.”[17]

Social media has likewise become a playground for AI hype, with numerous influencers suggesting that the transformation of entire industries due to generative AI is underway. Earlier this year, it came to light that AI companies are paying some influencers hundreds of thousands of dollars each to boost AI on social media.[18]

One would think that the revelation of the existence of an AI propaganda industry would instill a sense of caution, but, if anything, the velocity at which AI hype travels seems to be accelerating. In February 2026, a post went viral on LinkedIn and X by Matt Shumer, CEO of a startup called OthersideAI, claiming that self-improving AI had already arrived and had rendered many knowledge workers’ skills obsolete.[19] The post, titled “Something Big Is Happening,” racked up tens of millions of views and considerable credulous press attention[20] despite Shumer’s obvious conflict of interest and the fact that he had previously made false claims about AI capabilities.[21] Later that month, stock markets tanked after Citrini Research, a previously obscure market research firm, published a “report” discussing a purely speculative scenario where advanced AI agents displace millions of white collar workers in 2028.[22]

Press coverage of the Shumer and Citrini pieces illustrates how the news media has frequently fed into the AI hype cycle by publishing stories that uncritically repeat pro-AI messaging. A meta-analysis of media representations of AI concluded that they “are predominantly positive, using economic framing and giving voice to established, institutional and often economic stakeholders” while “critical perspectives and the limitations of AI technologies receive considerably less attention.”[23] According to journalism professor Rasmus Klein Nielsen, coverage of AI “tends to be led by industry sources, and often takes claims about what the technology can and can’t do, and might be able to do in the future, at face value in ways that contribute to the hype cycle.”[24]

Examples abound. An April 2023 60 Minutes segment reported as fact claims by Google executives that AI had learned Bengali despite not being trained on it. In reality, the system had trained on thousands of Bengali texts.[25] In July 2025, The Economist ran a cover story titled “The Economics of Superintelligence,” arguing that a future where superintelligent AI unlocked explosive economic growth was the “immediate, probable, [and] predictable” result of advances in AI,[26] despite the complete absence of evidence that superintelligence is attainable, or even a coherent concept.[27]

Stories with a more skeptical tone occasionally appear, such as Stretfield’s New York Times piece quoted at the beginning of this section. Unfortunately, the same outlets frequently repeat AI hype narratives without words of caution. The same week that the New York Times ran Stretfield’s article, it also published an op-ed by the CEO of “an A.I.-powered software acceleration platform.” Its headline (“The A.I. Disruption We’ve Been Waiting for Has Arrived”) and tone (“The simple truth is that I am less valuable than I used to be” and “No matter where you work, my hunch is this is coming for you”) were only slightly less breathless than that of Shumer’s essay.[28] The very same day, the Times released a podcast where Times tech reporter Kevin Roose predicted that within a year, “dramatically better” AI agents will be “full-fledged members of the workforce” such that “there will be this new kind of company that is emerging with AI work at the center of it, and I think that’s going to be a really fast growing part of the economy.”[29]

B. Anatomy of the bubble: Everything’s big but the revenues

Unsurprisingly, these wildly inflated expectations have driven speculative investment in AI — even though, the immense hype notwithstanding, generative AI companies have not figured out how to profit from the technology. The result has been a stark split screen: AI companies (1) enjoy unprecedented valuations while (2) burning through equally unprecedented amounts of cash with little to show for it. AI companies are increasingly resorting to questionable accounting methods, including some that are obviously deceptive, to inflate their revenues and mask rapidly growing piles of debt.

1. Valuations

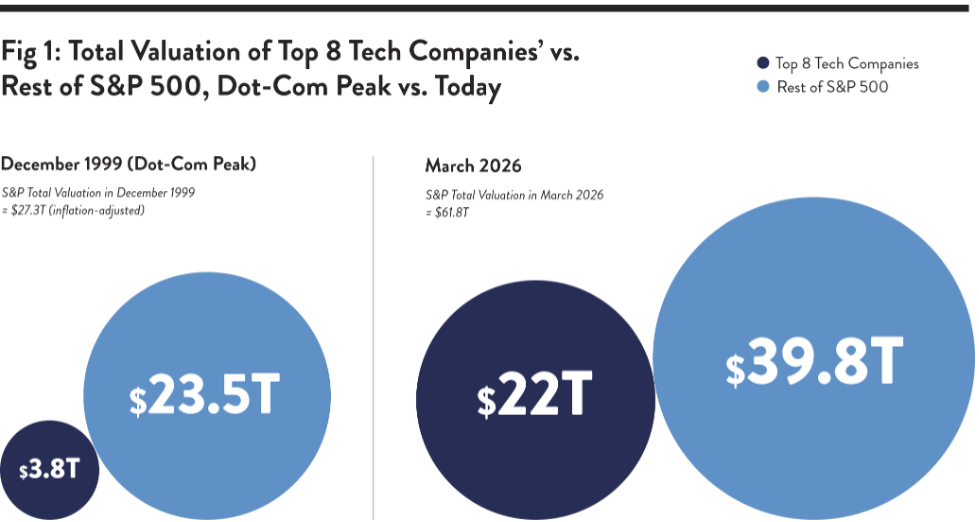

The stock market has never been as concentrated in a small number of closely connected companies as it is today. Currently, nine of the 10 most valuable companies in the world are tech companies (the 10th is Saudi Aramco), eight of which are based in the United States (the other is Taiwan’s TSMC, which manufactures AI chips). The eight U.S. companies (Nvidia, Microsoft, Apple, Alphabet, Amazon, Broadcom, Meta, and Tesla, in order of their market capitalization) are collectively valued at $22 trillion as of March 5, 2026, accounting for 36% of the S&P 500.[30]

By comparison, even at the peak of the dot-com bubble, only three of the top 10 global companies by market cap were U.S. tech companies, and the top eight U.S. tech companies at that time (Microsoft, Cisco, Intel, IBM, Oracle, Qualcomm, AT&T, and Verizon) combined to make up just 15% of the S&P 500’s total value, less than half the current share (see Figure 1).[31] One must go back to the mid-1800s, when railroads dominated equity markets, to find the last period of such extreme sectoral concentration.[32]

Today's biggest tech companies are also more interconnected than their dot-com era counterparts. In particular, today's tech giants are all deeply exposed to an LLM downturn. Among the eight largest companies in the country, six focus on either developing and deploying their own LLMs (Meta), providing goods or services to LLM developers (Nvidia, Broadcom), or both (Alphabet, Amazon, Microsoft). The other two (Apple and Tesla) are aggressively incorporating LLMs into their products and services.

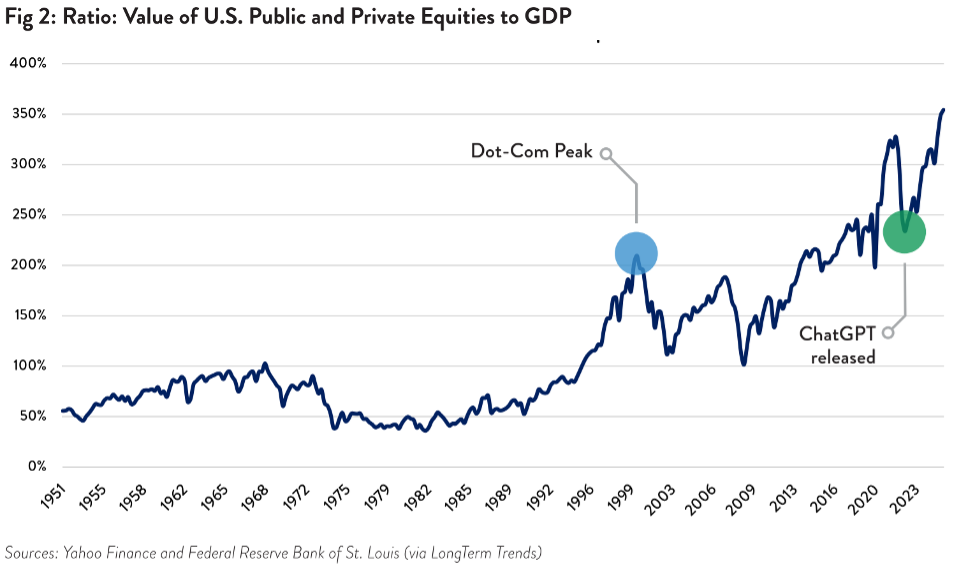

A stock market crash would likely have a bigger economic impact today than ever before. During the late 19th century railroad bubble, U.S. stock markets were worth less than half of U.S. GDP.[33] That ratio exceeded 100% for the first time during the run-up to the 1929 stock market crash and reached a new high of 150% at the peak of the dot-com bubble.[34] Today, that ratio is over 210%, having risen by over 70 percentage points since the launch of ChatGPT in November 2022.[35] That means U.S. stock markets are now worth more than double what the entire country produces in a year.

Additionally, roughly 60% of Americans own stock, more than at any point since records began, meaning that the economic pain from a stock market crash will directly affect more people than ever before.[36] By comparison, the stock ownership rate was just 10% at the time of the 1929 stock market crash.[37]

And that is just in the stock markets. OpenAI is still privately held, meaning that its shares are not sold on stock exchanges or otherwise available to the public, but it is more valuable than all but 15 companies in the world. The combined value of OpenAI ($840 billion) and Anthropic ($380 billion) tops $1.2 trillion,[38] more than any non-tech company in the world besides Saudi Aramco. Compare that to the dot-com era, when tech companies were also overhyped. When Amazon went public in 1997, it was considered massive for a private company at the time, with a valuation of $300 million (or $613 million in 2026 dollars).[39] That is not even one-tenth of one percent of OpenAI’s valuation today.

Combining both publicly traded and privately held companies, U.S. equities are now worth 354% of GDP, vastly higher than its previous dot-com era peak of 210%.[40] (See Figure 2)

2. Lots of spending (but little in revenues)

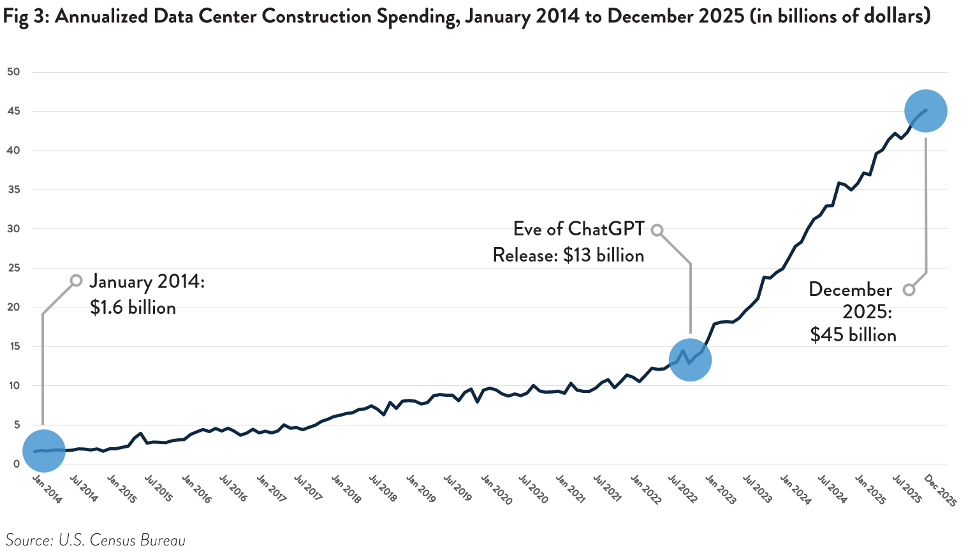

The exorbitant valuations of AI companies are accompanied by equally exorbitant spending on AI infrastructure. AI companies are splurging on data centers containing server racks filled with specialized chips that perform the complex calculations necessary to train and run generative AI models. In January 2014, the Census Bureau began tracking data center construction spending in the United States (see Figure 3).[41] That month, annualized[42] spending on data centers was $1.6 billion. That slowly rose to $13 billion in October 2022, the eve of ChatGPT’s release, before surging to more than $20 billion in November 2023, $30 billion in May 2024, and $40 billion in May 2025. In December 2025, the last month for which data are available, it crossed $45 billion — exceeding, for the first time, the amount spent on office construction.[43]

Data center spending is set to rise still further in the coming years, largely driven by so-called “hyperscalers,” the term for the huge corporations that are spending the most on chips, data centers, and related AI infrastructure. Just five such hyperscalers — Alphabet, Amazon, Meta, Microsoft, and Oracle — plan to spend $770 billion on data centers and related AI capital expenditures in 2026 alone.[44] By 2030, Deutsche Bank predicts that the total amount spent on data center infrastructure will reach $4 trillion, more than 10 times the inflation-adjusted cost of NASA’s Apollo moon-landing program.[45] About 75% of hyperscalers’ infrastructure spending goes toward AI-specific items like AI-optimized GPUs, servers, networking equipment, and data centers.[46]

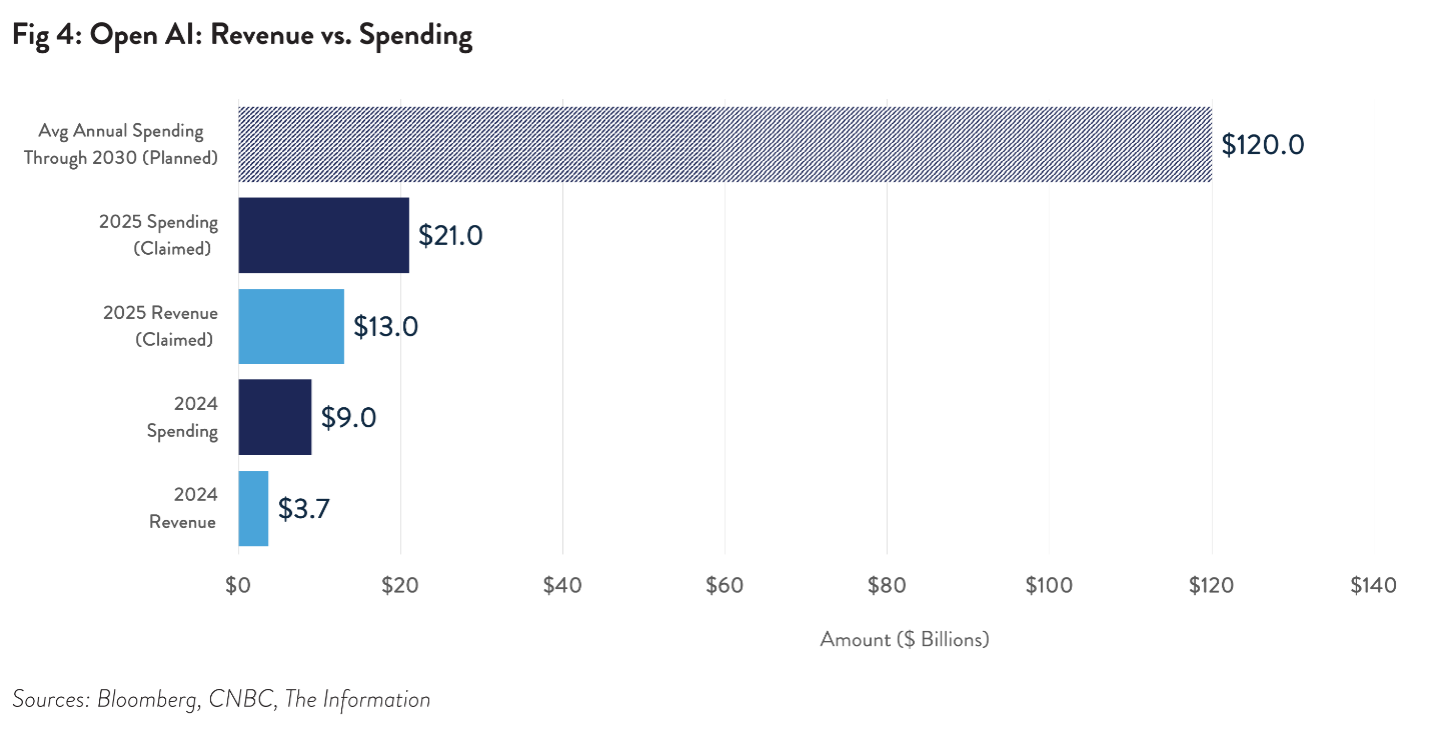

So far, however, the massive investments have not come close to generating any profits for the companies that make or sell AI tools. Generative AI has instead proven to be, in the words of technology writer Ed Zitron, a “cash incinerator.”[47] OpenAI claimed to have generated $13 billion in 2025, although there are ample reasons to question how much of this is revenue for actual AI services.[48] Reporting indicates that while 70% of OpenAI’s revenue comes from ChatGPT subscriptions, only 5% of ChatGPT users pay for the service.[49] This bodes poorly for OpenAI’s future revenue prospects because early adopters tend to be both more enthusiastic about a new technology and more willing to pay for cutting-edge features.[50] Nevertheless, OpenAI plans to spend an average of $120 billion per year on capital expenditures between now and 2030.[51]

The hyperscalers are likewise spending massive sums of money on AI infrastructure with little revenue to show for it. The five biggest hyperscalers (Alphabet, Amazon, Meta, Microsoft, and Oracle) earned an estimated $25 billion in AI-related revenue in 2025, just 4% of what they plan to spend on AI infrastructure in 2026.[52]

3. The debt deluge

How can an industry that appears to be bringing in 11 digits worth of annual revenue hope to cover 13 digits worth of spending on infrastructure? Until the fall of 2025, the AI boom was mostly financed through the enormous cash flows that tech giants draw from their pre-AI monopolies and oligopolies, supplemented by investments from venture capital and private equity funds. But as spending continued to rise without corresponding increases in revenue, AI companies began turning to debt — lots of it and from every corner of the financial system.

The explosion of debt in the AI ecosystem has become “all-consuming,” extending to every corner of debt markets.[53] The first 10 months of 2025 saw $125 billion in new debt tied to AI infrastructure projects, more than seven times the amount issued during the same period in 2024.[54] AI-linked companies have likewise issued nearly seven times as much in convertible bonds (a type of debt that can be converted to stock) during the first weeks of 2026 compared to the same period in 2025.[55]

Much of the borrowed money is also coming from private credit, a largely opaque and unregulated part of the debt market (sometimes called the “shadow debt” market). In these markets, private equity fund managers take the place of banks and the funds come from insurance companies, pension funds, and the ultra-rich. Private credit was a rounding error in the global financial system before the financial crisis, but it passed $1 trillion for the first time in 2020[56] and has more than tripled over the past six years to more than $3 trillion today.[57] About $800 billion of new private credit debt is projected to go towards building out AI data centers over the next three years.[58]

4. Funny accounting

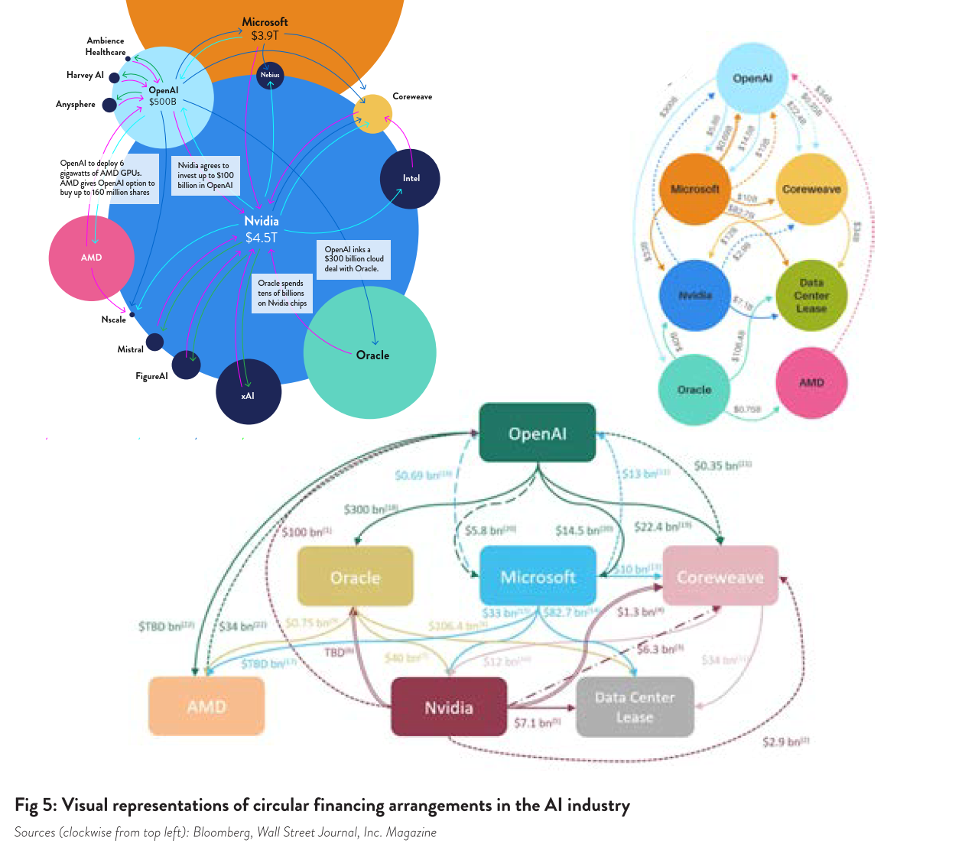

Historically, dubious accounting methods have been a hallmark of bubbles. Some accounting tricks make a company’s earnings appear much healthier (or much less troubling) than they actually are. During the dot-com bubble, companies started using circular arrangements (called “vendor financing”) where Company A pays Company B to buy Company A’s own products or services. This creates the illusion that both companies are generating new revenues when, in reality, they are simply passing the same money back and forth.

Other machinations can hide sources of risk — especially mounting debts. Just as circular financing can obscure paltry revenues, the use of shell companies (also called “special-purpose vehicles” or SPVs) can obscure reckless borrowing and spending. Enron infamously made liberal use of SPVs to hide debt before its bankruptcy, and Citigroup moved more than $100 billion to SPVs to conceal the scale of the bets it had placed on the housing market during the run-up to the 2007-2008 financial crisis.[59]

The AI industry is leaning on these techniques and adding a few of their own to obscure the shakier parts of their finances. The web of circular financing surrounding AI companies is a sight to behold — quite literally, in the sense that one must actually look at visual representations (such as those in Figure 5) of the incestuous relationships between the players in the AI ecosystem to begin to appreciate their extent. Such circular arrangements allow AI companies to report inflated revenues while making it more difficult to determine how much of their revenues come from selling actual AI-based products and services to businesses and consumers.

Shell companies are having another moment as well, with companies increasingly placing their AI-focused data centers (and the enormous loans used to finance them) in the hands of SPVs. Meta and Oracle are using SPVs to purchase chips and finance the construction of data centers without weighing down the balance sheets released to the public.[60] To build one data center, Meta worked with Morgan Stanley and private credit giant Blue Owl Capital to raise $30 billion in debt that is being parked in an SPV.[61]

Given the sheer magnitude of the gap between their revenues and their spending, however, AI companies are having to get even more creative. In recent years, Alphabet, Meta, Microsoft, and Oracle have extended the period over which they depreciate their AI chips, in essence claiming on their balance sheets that the chips will have a useful life of five to six years when they are, in reality, replacing the chips every two to three years.[62] That replacement cycle may be accelerating, with Nvidia now releasing new chips every year.[63]

By extending the depreciation period, companies can spread the cost of the chips over a longer period of time on their balance sheets, which makes it appear that they are spending far less each year than they actually are. Investor Michael Burry, who was among the first to recognize the mid-2000s housing bubble and was depicted by Christian Bale in the 2015 movie The Big Short, estimates that hyperscalers are using this technique to understate their expenses by a combined $176 billion over the next three years — with Microsoft (13%), Alphabet (14%), Amazon (21%), Meta (24%), and Oracle (48%) all overstating their profits by double digits.[64]

All these accounting tricks have been enabled by lax corporate transparency and accounting rules, which policymakers never fully addressed with legislation after the early 2000s Enron scandal demonstrated the ease with which corporations can manipulate the financial numbers they release to the public.[65] It is even easier for privately held companies like OpenAI and Anthropic to fiddle with their numbers because, unlike corporations traded on public stock exchanges, they need not release quarterly earnings statements reviewed by (at least theoretically) independent auditors. Instead, private companies can cherry-pick what numbers they release and when they release them. This allows, for example, OpenAI to report “revenues” by waiting until they have an unusually lucrative 30-day period, multiplying their revenues from that period by 12, and reporting the number as their “annualized” revenues — even if the reported number is far less than the company actually earns in any 12-month period.

Needless to say, companies rarely resort to these techniques if they are on solid financial footing; no one uses accounting tricks to hide healthy finances. The widespread use of such dubious accounting methods should be viewed as a major red flag for the AI industry’s financial health.

Part II: What are Bailouts?

The term “bailout” has maritime origins that still serve as a neat way of illustrating what the term means. In its original and most literal sense, “bailing out” is using a bucket to remove water from a boat that is becoming inundated. The idea is that by removing some of the water weighing the vessel down, the rescuers can preserve it until it can be repaired. Of course, if the damage is serious enough, the boat will sink despite the rescuers’ best efforts to bail it out. In that case, rather than wasting time and resources to keep the ship from sinking, it is best to focus efforts on saving the crew, salvaging whatever can be salvaged, and taking steps to ensure other ships don’t meet the same fate.

“Bailouts” in the economic sense operate much the same way, with the government (or, ultimately, taxpayers) taking the role of the bucket-wielding crew. In this type of bailout, emergency action is directed at preserving a company that otherwise would sink into bankruptcy. As with seafaring bailouts, whether an economic bailout effort succeeds depends in large part on the extent of the underlying damage. If a company has no obvious path back to profitability, it is best to let the company fail, salvage any valuable parts, and address the root causes of its demise.

A. Block framework

In 1991, in the wake of the savings and loan bailouts (discussed further below), Washington University law professor Cheryl Block wrote an article that identified and distinguished between overt and covert bailouts.[66] Overt bailouts involve government assistance explicitly designed to prop up a failing enterprise. Although the purpose of an overt bailout is apparent, its true costs often are not. For example, many overt bailouts have taken the form of loans or loan guarantees that leave taxpayers on the hook for any losses that a bailed-out company sustains while providing little or no potential upside if the company recovers.

Covert bailouts are subtler and less direct. They may include tax relief, protection from foreign competition, and exemptions from laws or regulations. Frequently, they are done through executive or agency fiat rather than through the legislative process. As Block notes, covert bailouts are insidious because, even more than overt bailouts, they tend to occur without significant voter awareness (much less input or debate) and are structured in a manner that disguises their true purpose and beneficiaries.[67]

Block identifies the “failing firm” defense to antitrust laws as a standardized form of covert bailout.[68] Under this defense, a merger that may harm competition and thus would ordinarily violate federal antitrust law — such as an industry giant buying up a competitor — may be permitted to proceed if one of the merging firms appears insolvent. This defense was first recognized by the courts and later incorporated into Department of Justice (DOJ) and Federal Trade Commission (FTC) joint antitrust guidelines, where they remain today.[69]

B. A brief history of bailouts

This section provides a concise history of bailouts to explore the forms bailouts can take and the justifications that bailout proponents offer for them. That history includes several recurring themes that will be explored in the remainder of this report. The history in this section is illustrative rather than comprehensive; thus, I gloss over some bailouts and don’t mention others.

1970s: Transportation and defense company bailouts

The bailout era began with a failed bailout push. The railroad industry had been in a decades-long decline that accelerated after the construction of the federally subsidized Interstate Highway System in the 1950s and 60s. By 1970, the debt-laden Penn Central railroad was teetering on the edge of bankruptcy. The railroad’s executives appealed to Washington for assistance. Bail-out proponents argued that Penn Central’s failure would threaten tens of thousands of jobs and cause cascading ill effects on the rest of the country’s rail transport network.[70] Despite support for a bailout from Nixon and the Federal Reserve, Congress refused to provide the necessary funding or loan guarantees, and Penn Central was forced to file for bankruptcy in June 1970. Congress then passed legislation aimed at salvaging the railroad’s useful assets, leading (among other things) to the establishment of publicly funded Amtrak in 1971.

Although Penn Central died, the idea of government bailouts did not. Lockheed Corporation, one of the country’s largest defense and aerospace manufacturers, was drowning in debt at the same time as Penn Central, but Lockheed was able to play the “strategic importance” card much more credibly than the railroad. Congress passed a law in August 1971 granting Lockheed $250 million in loan guarantees, equivalent to $1.9 billion in 2026 dollars.

With the federal treasury now seemingly available for failing enterprises to draw on, additional bailouts began to accumulate over the next decade. In 1979, Chrysler was still one of the nation’s largest car companies by volume, but it had been hit hard as rising oil prices led consumers to buy fewer and more fuel-efficient cars. With the company nearing bankruptcy, Chrysler approached Congress to request a bailout, citing the large number of job losses that would result from the company’s demise, especially in Detroit, where it was the largest employer. Congress passed a law providing Chrysler with $1.5 billion in loan guarantees, the largest bailout in history up to that point.[71]

1980s: The Savings and Loan Bailouts

An inflection point in the history of bailouts came with the 1980s savings and loan (S&L) crisis, after which bailouts aimed at entire industries became more common. S&Ls are membership-based financial institutions that historically focused on core consumer banking functions: offering interest-bearing savings accounts to consumers and using the resulting deposits to offer home loans and other essential consumer and household lending services. In 1980, S&Ls held $480 billion in mortgage debt, accounting for roughly half of all the home mortgages outstanding at the time.[72]

S&Ls’ traditional business model was risky, however, because of a mismatch between the time horizons on which the different parts of their business operated. Most of S&Ls’ income came from interest payments on mortgages, which typically have a fixed interest rate for 15 or 30 years. At the same time, they had to pay out interest on savings accounts, and those interest rates can change quickly. When interest rates rise, depositors expect higher interest rates on their savings, but the S&Ls could only raise interest rates so much before they started losing money (since the mortgages on their books still had the same lower interest rates as before). On the other hand, if they kept interest rates on savings accounts low, depositors might pull their money out and take their business to banks that offer higher rates.

In the late 1970s, the U.S. economy was buffeted by a rare combination of stagnating growth and high inflation, known as stagflation. The Federal Reserve eventually responded in 1979 by raising interest rates, choosing to tame inflation and thus bring prices under control even at the risk of triggering a recession. The resulting sky-high interest rates blew up the business model and threatened the solvency of many S&Ls.

The federal government first responded with a covert bailout. A 1981 law provided tax breaks to S&Ls that sold unprofitable loans and gave favorable tax treatment to strong S&Ls that took over their insolvent counterparts. The Reagan administration also loosened regulations that had been designed to ensure S&Ls do not make risky bets with their members’ savings. Far from resolving the crisis, however, this approach set the stage for a much larger one.

With minimal regulatory supervision, S&Ls attracted depositors by offering unsustainably high interest rates on savings, which they used to make ever-riskier (and sometimes outright fraudulent) loans.[73] When defaults predictably started to pile up on these loans in the late 1980s, many S&Ls once again faced insolvency. As the crisis intensified, regulators turned to more direct forms of assistance, offering loans and guarantees to investors willing to take over insolvent S&Ls.[74] But the rot ran too deep for these covert, firm-by-firm regulatory bailouts to stem the crisis, and S&L failures continued to accelerate.

Because the S&Ls played such a central role in financial markets, particularly through the hundreds of billions of dollars in mortgages they held,[75] widespread failures of S&Ls threatened the stability of the entire financial system. It was this risk of contagion that led Congress to step in for a second time.

The Congressional intervention that followed dwarfed all previous corporate rescue efforts. In 1989, Congress passed the Financial Institutions Reform, Recovery, and Enforcement Act. Among other things, the statute established the Resolution Trust Corporation, a government-owned “bad bank” that purchased the assets of failed S&Ls and either refinanced or sold them. Ultimately, taxpayers ended up paying $160 billion, or $380 billion in 2026, by the time the Resolution Trust Corporation ceased operations in 1995.[76] Many struggling S&Ls were scooped up by larger commercial banks, kicking off a wave of bank consolidations that continued through the 2008 financial crisis.[77]

2000s: Airline bailouts and consolidation

The next major federal government bailout was again aimed at an entire industry. Airline passenger bookings in the U.S. plummeted after the September 11, 2001 attacks, which involved four domestic airliners. With every major U.S. airline facing severe financial distress and uncertainty about when (or if) flyers would return, the commercial aviation industry faced collapse absent congressional action. It thus was and is hardly surprising that the airlines immediately approached Congress asking for a bailout.

In some ways, the 9/11 attacks were morbidly fortunate for the airlines. Most major airlines had been struggling for years before the attacks, starting shortly after the airlines were deregulated in 1978, a move that upended the industry and led to a vicious downward spiral of cost-cutting, deteriorating service quality, and lower profits.[78] Three major carriers (Pan-Am, Eastern, and TWA) went bankrupt in the decade before the 9/11 attacks and several others were barely treading water by the summer of 2001. When the airlines approached Congress with caps in hand after the 9/11 attacks, however, they were able to present themselves quite credibly as victims of an unforeseeable event from which few airlines would recover absent federal aid. In the words of Delta’s then-CEO, “almost no airline [was] strong enough to survive for long, facing the upcoming challenges.”[79]

Congress responded with a poorly drafted $15 billion bailout package that was both wasteful and largely ineffective. Billions of dollars in bailout funds ended up going to companies whose connections to the commercial aviation industry were tenuous at best, such as helicopter companies that ferried oil workers to rigs.[80] The billions of dollars of taxpayer assistance was also not enough to prevent Delta, Northwest, United, and US Airways (twice) from filing for bankruptcy over the next four years (American Airlines managed to hold on until 2011).

With the industry continuing to struggle and the public unlikely to tolerate another overt bailout, a period of consolidation followed that continues to this day. Between 2008 and 2013, each of the four largest carriers (American, Delta, Southwest, and United) purchased one of its smaller rivals (US Airways, Northwest, AirTran, and Continental, respectively). More recently, Alaska Airlines purchased struggling Hawaiian Airlines in 2024 after buying its West Coast rival Virgin America in 2016, making Alaska the dominant carrier along the Pacific Coast.

Consolidation returned the airlines to profitability (the four largest carriers were the world’s most profitable airlines from 2012 to 2016),[81] but with fewer choices for passengers, airline service quality deteriorated still further.[82] The airlines received another bailout during the 2020 COVID pandemic, even though the industry had paid out 96% of its free cash flow in share buybacks and dividends in the preceding decade rather than saving it for another downturn.[83] Apparently, the airlines had (correctly) surmised that they did not need to make their business resilient against shocks to the travel industry because, if it came down to it, the government would bail them out yet again.[84] And so it did.

2008: The Financial Crisis

The financial sector bailouts of late 2008 are what most people think of today when they hear the term “bailout,” but government assistance to the financial sector began more than a year earlier. The underlying crisis stemmed from the subprime mortgage market. “Subprime” refers to borrowers, such as those with poor credit or with little or no income, who pose a high risk of defaulting on loan payments. Banks had historically hesitated to give home loans to subprime borrowers, but that changed when a booming market arose for buying and selling huge packages of mortgages called collateralized debt obligations, or CDOs. The fees that lenders earned from writing new mortgages and then selling them so they could be packaged into CDOs were very lucrative. Consequently, lenders gradually lowered their lending standards and eventually started practically giving away mortgages even to subprime borrowers, often enticing them with low initial payments that did not reflect the true cost of the mortgage.

The market for subprime mortgages was enormous — in 2007, $1.3 trillion, or $2.1 trillion today, in subprime mortgages was outstanding, and the market for CDOs was even bigger ($2 trillion, or $3 trillion today). CDOs had been considered so safe that much of the financial system’s plumbing came to depend on them. But when subprime borrowers started defaulting on their mortgages in large numbers in 2007, the huge market that had built up around them came crashing down. When it did, credit markets began to seize up.

The Federal Reserve first attempted to get them unstuck by assuring banks that it would provide as much short-term credit as they wanted. But the financial sector was not merely experiencing temporary cash flow problems; rather, it was slowly sinking under the weight of hundreds of billions of dollars of bad loans they had collected on their balance sheets through years of reckless lending, much like the S&Ls two decades before. Many institutions simply did not have enough assets to cover their debts. In other words, the problem was one of solvency rather than liquidity.

The health of many financial institutions thus continued to deteriorate over the following months. The first major financial institution to face complete collapse was the investment bank Bear Stearns, which reached the precipice in March 2008. With hundreds of billions of dollars in assets under management and a web of connections with banks and other financial institutions, policymakers feared that Bear Stearns’s uncontrolled collapse would trigger a financial crisis.

With the investment bank’s cash reserves nearly empty and private banks refusing to lend to it, the Federal Reserve Bank of New York first attempted to rescue Bear Stearns with a bridge loan.[85] When this bailout failed to stabilize the firm, the Treasury Department and Federal Reserve brokered a deal where JPMorgan Chase, the largest U.S. bank, was permitted to purchase Bear Stearns, the fifth-largest investment bank at the time. As part of the deal, the Federal Reserve Bank of New York had to agree to absorb $30 billion of Bear Stearns’s losses, while JPMorgan chipped in just $1.4 billion.[86] In effect, the New York Fed paid the giant bank $30 billion to take over Bear Stearns, with the New York Fed (and thus, ultimately, taxpayers) assuming nearly all the risk.

The political blowback from the Bear Stearns rescue, along with the federal takeovers of Fannie Mae and Freddie Mac in August 2008, was central to regulators’ decision to hang Lehman Brothers (another investment bank) out to dry when it approached collapse. Lehman filed for bankruptcy on September 15, 2008. From there, the crisis spiraled. Almost immediately, markets turned on reinsurance giant AIG, which the Federal Reserve was forced to bail out at a cost of more than $270 billion in today’s dollars.[87] When the market panic continued to spread, Congress finally stepped in. Dusting off the playbook from the S&L crisis and adding a few new plays, the 2008 bailout legislation propped up the financial industry through a mix of cash injections, loan guarantees, and purchases of toxic assets.

There were occasional bursts of public outrage over the bailouts, particularly when it came to light that financial institutions had paid out tens of millions of dollars in dividends and share buybacks as well as bonuses and severance packages to executives immediately before,[88] during,[89] and right after the crisis.[90] But the revelations came out in drips and drabs, and many of the most outrageous examples only came to light months or years after the most acute phase of the crisis, which helped prevent public outrage from reaching the critical mass necessary for structural reforms.

Banks and other defenders of the 2008 bailouts often argue that, overall, taxpayers got their money back.[91] Many economists question the accounting methods used to claim that the bailouts were profitable.[92] Moreover, the rosy calculations never seem to account for the $787 billion stimulus package that Congress had to pass in 2009 to rescue the economy from the crisis created by the financial sector.

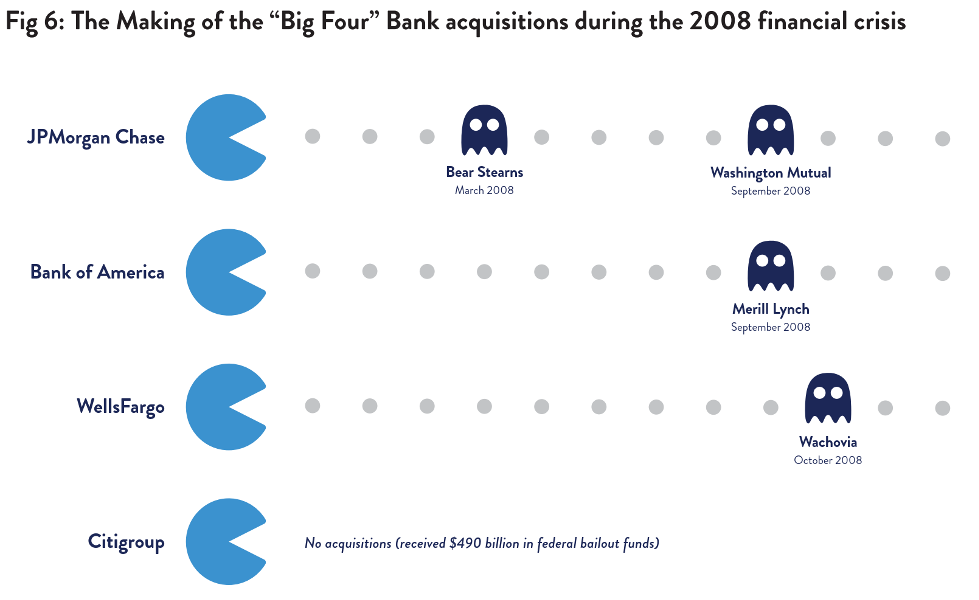

One thing that can be identified with certainty as an outcome of the 2008 bailouts was that the biggest banks became even bigger by purchasing or buying up the assets of their struggling rivals. In this case, the government did not merely stand aside as in the case of the mega-airline mergers. It actively encouraged the acquisitions and even helped negotiate some of them.[93] Between March 2008 and January 2009, JPMorgan Chase absorbed Bear Stearns and Washington Mutual, Bank of America purchased Merrill Lynch, and Wells Fargo merged with Wachovia.

Only Citigroup, then the world’s third-largest bank, was too weighed down by its exposure to the subprime crisis to scoop up any of its smaller rivals. Instead, Citi received nearly half a trillion dollars in federal bailout funds, much of it with no strings attached.[94] This was not only more than any other bank received during the crisis, but also more than the amount spent on all pre-crisis federal bailouts combined. Today, JPMorgan Chase, Bank of America, Citi, and Wells Fargo are the four largest banks in the country and dominate U.S. commercial banking, with more than $9 trillion in assets between them.[95] The smallest of the four (Wells Fargo) holds nearly triple the assets of the fifth-largest bank.[96]

2009: The GM and Chrysler Bailouts

The U.S. auto industry had continued to decline in the decades following the 1979 Chrysler bailout. The shocks of 2007-2008 provided the coup de grâce for Chrysler and General Motors (similar to the impact of the September 11 attacks on the struggling airline industry). By late 2008, it was clear that both companies were on the brink of bankruptcy.

The debate over whether to bail out the automakers was heated. Auto manufacturers are not banks, and their failures would not cause businesses to lose access to the funds needed to make payroll or consumers to lose access to the money they need to pay bills. But, as in the 1970s, GM and Chrysler did employ hundreds of thousands of people, mostly in union jobs with pension plans that could be wiped out in traditional bankruptcy. The companies’ collapse also threatened to have a cascading impact on the rest of the auto industry, including parts suppliers, dealerships, and auto loan specialists.

The federal government therefore stepped in, first by providing the two corporations with $25 billion in bailout funds using their authority under the legislation that bailed out the financial sector during the 2008 crisis.[97] When Chrysler and GM continued to deteriorate, the government orchestrated pre-packaged Chapter 11 bankruptcies, providing loans to help sustain the companies’ operations while they restructured their debts. The combination of federal financing and pressure meant that the Chapter 11 process, which can take years for companies far smaller and less complex than Chrysler and GM, was completed in a matter of weeks. The two corporations ultimately received a total of $80 billion in federal bailout funds.[98]

2023: The Tech Bank Bailout

In his 2018 book Last Resort: The Financial Crisis and the Future of Bailouts, University of Chicago law professor Eric Posner lays out two paradigmatic examples of bank runs. The first type of bank run (call it a “depositor-led” bank run) starts with depositors. For example, say a local bank operated in a small town where the local factory had just closed. Due to their sudden loss of income, many of the bank’s depositors may be forced to draw down their savings quickly to pay their bills and meet other immediate needs. Knowing this, the other depositors may seek to withdraw their money as well out of fear that the bank will run out of money. That fear may become a self-fulfilling prophecy, since each withdrawal makes the bank’s inability to meet its obligations more likely, thus spurring still more depositors to withdraw their funds.

The second type of bank run (call it a “fear-of-failure” bank run) starts with fears surrounding the bank itself rather than its depositors. If a bank gets bad press or otherwise experiences something that shakes people’s confidence in it, depositors may withdraw their funds not because they need the cash right away, but because they fear the bank will go under and take their money with it. Once this panic starts, the remaining depositors start to withdraw their funds as well in a downward spiral similar to bank runs that start with distressed depositors.

Bank runs of both types have become much less common over time. Banks dependent on a small number of similarly situated depositors, like a factory town’s local bank, have become much rarer as people moved to larger metropolitan areas and local banks gave way to regional and eventually national and international banks. Moreover, the United States government insures all bank deposits up to $250,000 per account through the Federal Deposit Insurance Corporation (FDIC). That means that 99% of bank accounts are fully guaranteed by the federal government even if the bank that houses them fails.[99] Consequently, few depositors have any reason to fear they will lose their money even if they think their bank is about to go bust.

Leave it to the tech industry to make bank runs great again.

In 2023, four regional banks with close ties to Silicon Valley failed in rapid succession, falling prey to both types of bank runs. It started with Silvergate Bank, over 90% of whose deposits were linked to the cryptocurrency industry.[100] Silvergate was the primary bank for the fraudulent crypto exchange FTX, whose demise in late 2022 triggered a cryptocurrency collapse.[101] Crypto firms and their investors were forced to withdraw their money, leading to a depositor-led bank run. Silvergate failed on March 8, 2023.

Silvergate’s demise immediately triggered a run on Signature Bank, at the time a well-regarded regional bank with a reputation for scrappiness and providing services to overlooked neighborhoods and businesses — until, that is, it started soliciting crypto clients.[102] The crypto sector eventually became central to the bank’s business and reputation. Signature saw high outflows of depositors after the late 2022 crypto crash (another depositor-led bank run) that became a flood after Silvergate’s failure made depositors fear for the bank’s solvency (a fear-of-failure bank run).[103] The FDIC seized Signature Bank on March 12.

The other two failed banks, Silicon Valley Bank (SVB) and First Republic Bank, were based in the San Francisco Bay Area and focused on providing services to wealthy Silicon Valley clients. Both banks suffered from the same pair of flaws. First, they held billions of dollars in long-term bonds and mortgages that they had purchased when interest rates were low. This meant that, like the S&Ls in the 1970s, their balance sheets got weaker as interest rates rose. Second, the vast majority of both banks’ deposits were uninsured because they were above the $250,000 FDIC limit. Deposits above that limit are treated like any other debt in bankruptcy, which means depositors with seven-figure account balances would have ended up at best losing access to most of their funds for an extended time[104] and at worst losing their uninsured deposits altogether.[105]

These flaws combined to doom SVB and First Republic in the wake of the 2021-2022 inflation surge. As a result of the first flaw, the banks ran into trouble when the Fed started raising interest rates in 2022. As a result of the second, the banks’ wealthy clientele began withdrawing their funds once the banks’ fragility became known, leading to a fear-of-failure bank run.[106]

SVB was the first to fail. When the FDIC took over SVB on Friday, March 10, 2023, many of the bank’s wealthy Silicon Valley clients still had significant balances in SVB accounts. Over the following weekend, some of those clients began pressuring the Biden administration and Federal Reserve to guarantee all of SVB’s deposits without regard to the FDIC limit; “their rhetorical strategy of choice was to insist that unless SVB’s depositors were made immediately whole, the entire tech industry and every non-megabank in America would be at risk.”[107]

The regulators caved, agreeing on the evening of Sunday, March 12 to guarantee all SVB deposits, including those above the FDIC maximum.[108] This set the stage for another bank, First Citizens, to purchase SVB’s book of business at a discount two weeks later, with the FDIC absorbing an estimated $20 billion of SVB’s losses as part of the deal.[109] This was, in essence, a covert $20 billion bailout of the multimillionaire and billionaire venture capital and tech entrepreneurs who had millions of dollars each in uninsured SVB deposits.

Just as the collapse of Silvergate begat the run on Signature, the collapse of SVB triggered the run on First Republic. When First Republic failed seven weeks after SVB, its assets were sold to JPMorgan Chase, the largest U.S. bank — and the same bank that absorbed Bear Stearns and Washington Mutual during the 2008 financial crisis. Far from attempting to block a sale that made the country’s biggest bank even bigger, federal regulators (again) actively facilitated it.[110]

2025: Covert private equity bailout

In August 2025, President Trump issued an executive order directing regulators to relax the rules that protect workers’ 401(k)s and other retirement accounts from being sucked into opaque private markets.[111] The title of the order is “Democratizing Access to Alternative Assets for 401(k) Investors.” In other words, the administration framed the change as an investment opportunity for workers.

In reality, these changes are not intended to help workers, but rather to rescue private fund managers who, despite their immense wealth and economic power, are increasingly desperate to recruit new investors. As with the tech banks, albeit to a less extreme degree, many private equity and credit funds have underperformed since the Fed raised interest rates in 2022.[112] Fund managers cannot cash out investors in those existing funds, much less convince those investors to invest in new funds (including in the red-hot AI market) unless they can find new investors to pay off the old.

Indeed, the same week Trump issued his executive order, Bloomberg reported on private equity and credit firms’ rising use of so-called continuation vehicles (CVs), which are supposedly “new” funds but actually contain underperforming assets from one or more of a private capital firm’s existing funds.[113] Having put old fund wine into a new CV wineskin, the private capital firm recruits new investors to invest in the CV and then uses the proceeds to pay off the old fund’s investors. In some cases, the CVs have themselves underperformed, forcing fund managers to create CVs for CVs. I leave it to readers to decide for themselves just how closely this resembles a Ponzi scheme.

For now, the point is that the CV strategy only works as long as new investors can be recruited. That is why American workers’ retirement accounts are so attractive: they represent the largest untapped pool of potential new investors, with 70 million workers holding $12.5 trillion in retirement accounts.

In the months since the executive order, more and more cracks have appeared in the private capital ecosystem. A rising number of private capital firms have seen the equivalent of bank runs on their funds and have been forced to limit how much investors may withdraw to keep those funds from collapsing.[114]

The private equity industry had conducted a sustained lobbying campaign to push for regulatory changes that would open workers’ retirement accounts to them.[115] That the slow-motion crash in private capital markets came so soon after the executive order is strong evidence that the order was about plugging holes in private equity firms’ funds, not providing workers with investment opportunities. If the executive order is implemented and these firms’ shaky funds continue to stagnate or deteriorate, workers and retirees will increasingly be left holding the bag.

C. Bailout consequences: The big get bigger and the rich get richer

Readers will note a recurring theme in the above history: the government often allows, and in many cases actively encourages, large monopolistic and oligopolistic companies to take over struggling smaller ones. Indeed, such pairings increasingly seem to be the federal government’s first resort in a crisis, with regulators arranging them so quickly and eagerly that antitrust considerations — such as whether the elements of the failing-firm defense have been satisfied — appear not to enter the calculus. As Block wrote, such acquisitions are a form of covert bailout.[116] Worse, these shotgun marriages have generally not been accompanied by efforts to ensure that the mergers would not harm workers or consumers, much less by legal reforms to mitigate the need for future bailouts.

The core danger of monopoly is the power to exploit workers, businesses, and consumers and abuse political processes for corporations’ private ends. Previous Open Markets Institute publications have analyzed how monopolistic Big Tech companies are using their power to capture any new markets that AI unlocks and appropriate the gains for themselves.[117] The history of bailouts reveals the other side of that coin: when gains fail to materialize and an industry instead experiences a collapse or crash, powerful companies can still use their market power to entrench their dominance by ensuring that they benefit from any subsequent bailouts.

Another frequent consequence of bailouts is that the already wealthy executives of bailed-out corporations somehow end up still wealthier. Typically, bailouts (including the S&L, airline, and financial crisis bailouts discussed above) include some short-term restrictions on new executive compensation and golden parachutes — that is, huge severance packages that some executives receive when they are fired — as well as payments to shareholders like dividends and buybacks. But such legislation typically does not make the voiding of existing compensation agreements a condition of federal assistance.

For example, while the October 2008 financial sector bailout prohibited “any new employment contract with a senior executive officer that provides a golden parachute,” it allowed executives to collect any golden parachutes they had been granted under existing severance agreements.[118] GM CEO Rick Wagoner thus was able to walk away with a $20 million golden parachute in March 2009 after presiding over the demise of his company, which had previously accepted more than $17 billion in bailout funds and would file for bankruptcy two months later.[119] The 2001 airline bailout legislation was even more generous to executives, merely requiring that executives not receive pay increases for two years after receiving bailout funds.[120] Bailouts by the Federal Reserve often contain no meaningful restrictions, as exemplified by the more than $165 million in “retention bonuses” that AIG executives and financial services employees received just months after being bailed out.[121]

Because such payments often enrich people who played a role in the business failures and crises that necessitated the bailouts, they are particularly corrosive to public trust, creating the (not unjustified) perception that the goal of bailouts is to protect the interests of the wealthy and powerful rather than to benefit the economy as a whole. But these incidents of unjust enrichment tend to come to light only after public consciousness has moved on from the underlying crisis. As a result, the bursts of outrage have not yet translated into meaningful legislation to prevent the enrichment of bailed-out executives, much less the systemic changes that would be needed to prevent bailout conditions from arising in the first place.

D. Bailout justifications

As the above history illustrates, those seeking to obtain or justify a bailout usually offer two types of arguments:

(1) Importance: The firm or industry is important enough to warrant government action to preserve it. The most common variations of this justification are that the firm or industry is too big to fail or that its collapse would cause contagion through other parts of the economy. Either way, the implication is that the collapse would seriously harm ordinary people and the real economy.

(2) Worthiness: The firm or industry is worth preserving. The most common variations of this justification are that the firm or industry is fundamentally solvent and is simply facing temporary cash flow challenges and/or that it is the innocent victim of some unforeseeable event or circumstance.

1. Importance arguments

Bailouts are never cast as being primarily for the benefit of the bailed-out firms. Instead, proponents invariably frame each bailout as a necessary step to prevent severe negative consequences extending well beyond the bailout’s direct beneficiaries. The crux of a too-big-to-fail argument is that the bailed-out company or industry is systemically or strategically important, such that its failure would directly lead to severe consequences for the nation’s economy or security, even if its failure would not affect other companies or industries. The rescue of Lockheed in 1971 provides perhaps the purest example of this justification. The argument was not that Lockheed’s bankruptcy would cause an economic panic or lead to a cascading sequence of other ill effects. Rather, maintaining the nation’s largest defense contractor as a going concern was seen as essential to the country’s security in and of itself.

A contagion argument focuses not on — or at least not only on — the immediate consequences of a company or industry’s collapse, but on the possibility that such a collapse would start a chain reaction of other negative impacts. This argument is particularly potent in financial crises. The failure of a large bank poses systemic risk not just due to the sheer scale of its assets and liabilities but also because large banks constantly do business with many other financial institutions. As a result, banks tend to hold lots of other banks’ assets at any given time. Because assets are frozen in bankruptcy, it’s not just the bank’s clients that may lose access to their assets when a bank fails, but the clients of any other financial institutions that had the misfortune of doing business with it.

Too-big-to-fail and contagion arguments are often closely linked. The larger the bank, the more interconnected it typically is with other banks, which means that bigger banks both are more important in themselves and create bigger risks of contagion. Proponents of the 2009 auto industry bailouts also leaned on both types of arguments. Chrysler and GM employed hundreds of thousands of workers and supported the economies of a number of cities and towns (too big to fail) and there was a risk that their failures would spark an even larger auto industry meltdown (contagion).

That said, the history of bailouts demonstrates that those seeking bailouts often advance arguments that lie somewhere between dubious and absurd. Consider the 2023 tech bank meltdown. SVB and the other tech-linked banks that failed with it in the spring of 2023 clearly were not too big to fail. True, the SVB and First Republic bank failures were the largest since the 2008 financial crisis. But collectively, the four failed banks had a market share of just 2.5% among U.S. commercial banks, and their combined assets were less than one-quarter of Wells Fargo’s, the smallest of the Big Four.[122]

The tech bank failures also posed no real risk of contagion. Financial sector contagion typically arises when large numbers of interconnected institutions have large holdings of the same toxic assets. That was the case during the S&L and subprime mortgage crises, but not during the tech-oriented bank failures of 2023. Unlike Silvergate and Signature, few banks were dependent on business from crypto companies.[123] The vast majority of banks also did not have business models based, like SVB’s and First Republic’s, on interest rates remaining perpetually near zero or balance sheets that depend on a small number of ultra-rich clients parking huge amounts of uninsured deposits with them. Nearly 90% of SVB’s deposits were above the FDIC limit at the time of its failure, double the national average in 2022.[124]

The tech banks were notable primarily because of the wealth and political influence of their clients. It was that power and influence, not any realistic chance that their failures would affect the broader economy, that led to the bailout of SVB’s tech millionaires and billionaires.

2. Worthiness arguments

Turning to the other category of bailout justifications, one common worthiness argument is that the bailed-out business is fundamentally sound (or solvent) but is temporarily short on cash (or illiquid). The distinction between rescuing a firm that is illiquid and one that is insolvent is akin to that between attempting to bail out a ship that can be repaired and one that will sink regardless.

Solvency arguments are important for reasons of both fiscal prudence and democratic accountability. From a financial perspective, the government should be able to structure a bailout of a solvent firm in a way that allows taxpayers to (eventually) get their money back. That allows the intervention to be spun as less a bailout than an investment. Conversely, bailing out a firm that is insolvent, and thus likely to fail anyway, wastes taxpayer funds and makes the assistance look less like a bailout and more like good old-fashioned corporate welfare.

Another common type of worthiness argument asserts that the bailed-out company is an innocent victim of some unforeseeable external event or circumstance. These innocence arguments are particularly important when the bailout includes no-strings-attached grants of money to the bailed-out firm or its creditors and shareholders.

An archetype for an “innocence” argument would be the Paycheck Protection Program (PPP) passed in the aftermath of COVID, which allowed virtually all small businesses to stay afloat during the peak of the pandemic as long as they did not lay off their workers. The recipients of PPP funds neither caused nor could have reasonably foreseen the pandemic. Additionally, most had good solvency arguments — although no one knew how long the crisis would last, it was correctly assumed that most businesses would eventually recover once it ended.

Worthiness arguments are also often quite weak. Companies seeking bailouts frequently attempt to blur the already hard-to-discern line between insolvency and illiquidity, attempting to make their critically damaged ships seem seaworthy. Many do so by framing the crisis that threatens to drive them into bankruptcy as a transient event that makes their assets appear less valuable than they actually are. Thus, such companies argue, they will eventually recover and be profitable again as long as they get government assistance.

Using this logic, numerous financial institutions requested and received bailout funds during the 2008 financial crisis even though their assets were worth far less than their liabilities on the open market, with no guarantee of when or if they would recover. Up to and even past the bitter end, many executives and shareholders of Bear Stearns and Lehman Brothers refused to accept that their firms were insolvent. Each claimed that they were the victims of short sellers (investors who identify overpriced companies and bet that their stock will go down) and that their assets would eventually rebound in value once the market panic subsided.[125]

Remarkably, despite being deeply involved in the reckless, opaque practices that gave rise to the crisis, they also proclaimed their innocence. In addition to blaming short sellers, financial firms pointed to risk models that they had developed to argue that the nationwide decline in housing prices that followed the collapse of the subprime market had been an unforeseeable event.[126] But the models’ failure was quite foreseeable. Most of the models only went back a few years, far less than the term of a typical fixed-rate mortgage and not long enough to capture any serious financial crisis.[127] The firms that deployed them ignored both the historical fact that housing prices had declined nationally in earlier historical periods and the common-sense economic principle that no asset is likely to increase in value forever.[128]

The 2023 bailout of Silicon Valley Bank’s wealthy depositors again provides an example of a bailout that occurred despite any plausible worthiness arguments. SVB clearly was insolvent, having already been seized by the FDIC at the time regulators decided to guarantee all the bank’s deposits. At that point, there was not even a boat left to salvage, rendering the guarantee a giveaway that benefited only a handful of wealthy depositors with account balances above $250,000, a level that meant that their bank accounts contained more than double the median American’s net worth.[129]

Moreover, the Silicon Valley executives and venture capitalists whose wealth was rescued by the covert bailout played a key role in accelerating SVB’s failure. Venture capital industry newsletters, emails, and social media posts during the run-up to SVB’s collapse fueled speculation about SVB’s imminent failure, making its rapid and chaotic collapse something of a self-fulfilling prophecy.[130] Researchers concluded that this likely accelerated SVB’s demise.[131]

Nevertheless, SVB’s wealthy clients had political cachet and were able to scare federal officials into believing that the stability of the financial system depended on bailing them out. That raises a disturbing question: If tech billionaires were so easily able to obtain a bailout of their preferred bank, what could they convince policymakers to do if the entire tech sector faced collapse?

Part III: Rebutting (and Prebutting) the AI Industry’s Bailout Arguments

Having reviewed the ingredients for an AI downturn and the nature and history of bailouts, it is time to turn to the question of what bailout arguments we can expect tech companies to make if, or rather when, a significant AI downturn arrives. We need not speculate as to some of these arguments because a stealth AI bailout movement may already be underway, as suggested by the quotes from David Sacks and Sarah Friar in the introduction to this report.[132]